Understanding Your Military Pension: How It Shapes Financial Decisions After Service

Abstract

For many service members, the military pension serves as the foundation of their financial life after retirement. While most understand how the pension works, fewer recognize how it should drive decisions around investing, insurance, and retirement planning. The real value lies in integrating this income into a broader, coordinated financial strategy.

How the High-3 Pension Works [Simplified]

Under the High-3 system:

- Pension = 2.5% × Years of Service × Average of Highest 36 Months of Base Pay [1]

- Paid monthly for life

- Adjusted annually for inflation [COLA]

Blended Retirement System [BRS] & What’s Different

For those under BRS:

- Pension multiplier is reduced: 2.0% × Years of Service [2]

- BUT includes:

- Government TSP contribution match, up to 5%, between the 2nd and 26th year of service

- Continuation pay mid-career

What this means:

- Smaller guaranteed pension

- Greater reliance on:

- TSP

- Personal investments

Calculator Resource

Why Your Pension Changes Everything

The pension isn’t just income; it fundamentally reshapes your financial strategy. Even the BRS system, which exists as a reduced pension amount, gives a lifetime of financial foundation that completely changes the planning strategy when compared against traditional financial planning.

1. It Reduces Investment Risk

Guaranteed, inflation-adjusted income, like a pension, acts as a built-in stabilizer within your financial plan. Instead of relying solely on a traditional stock-bond mix to manage risk, the pension can serve as the “income-producing” portion of the portfolio. This allows the remaining investments to be positioned more efficiently for long-term growth.

2. It Impacts Your Retirement Number

Most people ask, “How much do I need to retire?”. However, with a pension, the better question is, “How much income do I still need beyond my pension?”.

3. It Influences Your TSP Strategy

Your pension often allows you to take a more growth-oriented approach. Retired military should think differently about withdrawals, Roth vs traditional decisions, and long-term compounding.

4. It Affects Your Insurance Decisions

Because your spouse may already have a base level of guaranteed income through your pension, protecting that income stream becomes a key consideration. Additionally, life insurance needs may shift, focusing more on covering current obligations.

5. It Creates Tax Planning Opportunities

During transition, you may have lower taxable income, providing flexibility to perform Roth conversions and reposition assets for a better long-term strategy. [3] It is worth noting that eligible retirees can further reduce the tax burden on their military pension by qualifying for Combat-Related Special Compensation [CRSC]. [4]

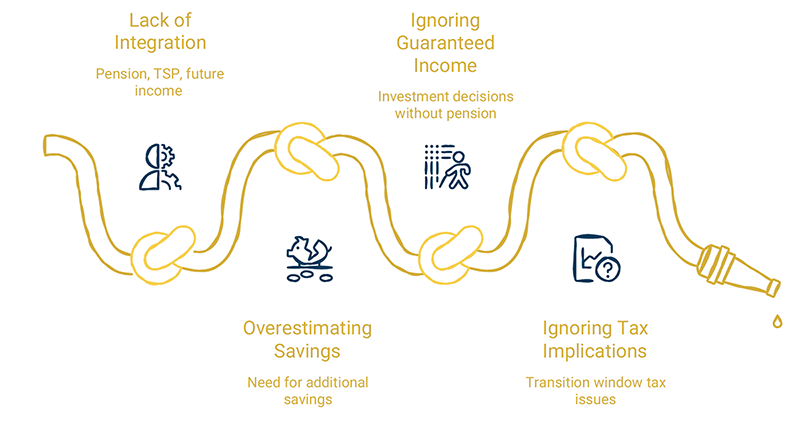

Where Mistakes Typically Happen

Final Thought

The right approach depends on how your pension fits alongside your TSP, taxes, civilian income, insurance decisions, and long-term goals. As discussed in our Survivor Benefit Plan [SBP] for Retiring Veterans: Pros and Cons | Bay Capital Advisors article, decisions surrounding pension protection, life insurance, and income planning are all interconnected.

If you’re within a few years of transition and want to better understand how these decisions fit together within your overall financial framework, please click the link below or book a quick financial review at carey@baycapitaladvice.com or calendly.com/careypeekstok.

Resources

- [1] Department of War. [2026] Comparison Chart of Regular and Non-Regular Retired Pay. Retirement

- [2] Department of War. [2026] Blended Retirement System. Retirement

- [3] Smart Asset. [May 2026] Is a Roth IRA Conversion Really Worth It? Is a Roth IRA Conversion Really Worth It?

- [4] U.S. Department of Veterans Affairs. [2026] Combat-Related Special Compensation [CRSC]. Combat-Related Special Compensation [CRSC] | Veterans Affairs