Thrift Savings Plan (TSP) Strategy for Transitioning Military: Key Considerations

Abstract

The Thrift Savings Plan (TSP) is one of the most valuable retirement assets available to military

members and federal employees. As you transition out of service, decisions around how to manage your TSP can have long-term implications for taxes, investment flexibility, and retirement income. This document outlines the key advantages, limitations, and decisions to consider when evaluating how your TSP fits into your broader financial strategy.

Advantages of the Thrift Savings Plan

Low-Cost Investment Structure

One of the primary advantages of the TSP is its extremely low expense ratios compared to most private investment options. In fact, the fund with the highest ratio within the options of the TSP boasts an expense ratio of 0.051%, or 51 cents for every $1000 dollars invested.1

Ability to Remain in the Plan After Separation

As long as participants have at least $200 in the account, you are not required to move your TSP funds upon separation from service.2

You can:

- Keep your assets within the TSP

- Continue to manage investments

- Allow long-term growth within a familiar structure

Access to Additional Retirement Rollovers

Even after separation, you may still consolidate retirement assets by rolling eligible funds into your TSP account. This can simplify account management and maintain cost efficiency. 3

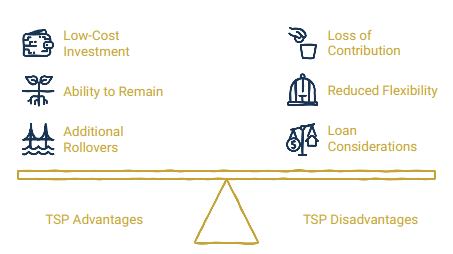

Thrift Savings Plan Advantages

Disadvantages and Limitations of the TSP

Loss of Contribution Ability After Separation

Once you leave federal or military service, you are no longer able to make direct contributions to your TSP. This limits your ability to continue building the account through earned income.

Reduced Flexibility Compared to IRAs

While the TSP offers simplicity and low costs, it has:

- Limited investment options

- Less flexibility in withdrawal strategies

- Fewer customization opportunities compared to private accounts

Loan Considerations at Separation

If you have an outstanding TSP loan at separation, you must decide to:

- Repay the loan before separation or within 90 days 4

- Continue payments

- Or allow it to be treated as taxable income

Note: Failure to manage this properly can create unexpected tax consequences.

Weighing TSP Advantages and Disadvantages for Transition

Key Decisions at Transition

1. Keep TSP vs. Rollover to an IRA

At separation, one of the most important decisions is whether to:

- Keep funds in the TSP

- Roll them into an IRA

- Transfer into a new employer plan Each option has trade-offs related to:

- Cost

- Investment flexibility

- Long-term strategy

2. Withdrawal Strategy and Timing

After separation, you have multiple options for accessing your funds:

- Partial withdrawals

- Full distribution

- Installment payments

- Annuity purchase

Note: Early withdrawals may be subject to penalties before age 59½ 5

3. Tax Planning Considerations

The transition period often creates:

- A temporary drop in taxable income

- Opportunities for Roth conversions

- Strategic withdrawal planning

This is one of the most important windows for long-term tax efficiency.

Conclusion

The Thrift Savings Plan (TSP) is a powerful and cost-effective retirement tool, particularly during your military career. However, the decisions you make at transition, whether to keep, move, or restructure your account, can significantly impact your long-term financial outcomes.

Like most financial decisions, there is no one-size-fits-all answer. The right approach depends on how your TSP fits within your broader financial plan, including your pension, taxes, and future income strategy.

If it’s something you’ve been thinking about and want a second perspective, book a complimentary financial review at https://calendly.com/careypeekstok.

Sources:

- Thrift Savings Plan (2026) Expenses and Fees. Expenses and fees | The Thrift Savings Plan (TSP)

- Thrift Savings Plan (2026) Leaving uniformed services. Leaving the Federal Government

| The Thrift Savings Plan (TSP)

- Thrift Savings Plan (2026) Move money into the TSP. Move Money Into the TSP | The Thrift Savings Plan (TSP)

- Thrift Savings Plan (2026) Leaving uniformed services. Leaving Uniformed Services | The Thrift Savings Plan (TSP)

- Internal Revenue Service. (2026) IRS Code Section 72(t). Substantially equal periodic payments | Internal Revenue Service